The US and the UK Master’s Part / Chapter-wise Dissertation Writing Service

Then You’ve Certainly Reached the Right place

Asset Pricing Model

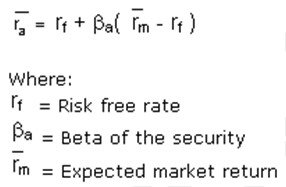

Capital Asset Pricing Model

The model discusses the association that exists between the risk as well as the expected return that is utilized in the deciding of the securities prices at risk.

The common theme behind the Capital Asset Pricing Model is that a potential investor could be compensated in the following ways- the risk associated and the time value of the money.“The time value of money is represented by the risk-free (rf) rate in the formula and compensates the investors for placing money in any investment over a period. The other half of the formula represents risk and calculates the amount of compensation the investor needs for taking on additional risk. This is calculated by taking a risk measure (beta) that compares the returns of the asset to the market over a period and to the market premium (Rm-rf)”. The site of Investopedia offers an explanation for the Capital Asset Pricing Model as follows: “The CAPM says that the expected return of a security or a portfolio equals the rate on a risk-free security plus a risk premium. If this expected return does not meet or beat the required return, then the investment should not be undertaken. The security market line plots the results of the CAPM for all different risks (betas). Using the CAPM model and the following assumptions, we can compute the expected return of a stock in this CAPM example: if the risk-free rate is 3%, the beta (risk measure) of the stock is 2 and the expected market return over the period is 10%, the stock is expected to return 17% (3%+2(10%-3%)).” The following review focus on the comparative overview of the other existing models.

The Fama-French Model:

The model proposed by Fama-French conclude theat the there is a positive and simplistic association between the market beta and the average returns during the initial years of the CRSP- NYSE file returns. However, this simplistic association could not be observed in the case of the contemporary period of the 1990s. Moreover, the association between beta and the average returns is not strong in the last five decades of the returns on the stocks of the NYSE. Thus the findings of Fama and French are inconsistent with that of the SLB models which support the hypothesis that the returns of stocks are positively associated with the beta value.

The work done by Banz supports a negative association between the size o f the company and the return of averages whereas Bhandari did the work show that the average return has a positive association with the leverage. Also, Basu’s work advocates a positive association between the E/P and the average return. A positive association between average return with that of the book to market equity is suggested by the statement in the case of stocks in America. In the case of the stocks in Japan, the BE/ME is also considered as a strong variable for the explanation of the average returns by Chan and co-workers.

The scaled drafts of the price of the stock of a company are the following variables: Leverage, size, a book to market equity and the E/P. These variables can be seen the light of getting the required information from the prices of the stock about the predicted returns of the stock. It is perfectly sensible to predict that some are repeated for the explanation of the average returns as they are the scaled drafts of costs. The main finding of the model is that the observations differences in the average stock returns related to leverage, size, a book to market equity and the E/P are captured by the size, period and the book to equity.

Fama-French model and asset pricing theory:

The results are consistent with the theory of asset pricing in the following sense. As the intercept of the FM is supposed to be similar for all the stocks, a linear architecture on expected returns and returns is imposed by the FM regressions. A “rational asset pricing frame work” on the association between the book to market equity, average return and size is predicted by this model.

Though the interpretations proposed by this model are perfectly at par with the theory of asset pricing, the theory is not enough to explain the economic discrepancies.How can the part played by the book to market equity and size be explained regarding economic perceptions?. The following are the suggestions put forth by Fama and French.

Assessing the association between the returns of the portfolios and the variables that estimate the differences in the conditions of the business can assist in the exposure of the qualities of the economic risks as shown by the book to market equity and the size.

The theory put forth by Chan and other workers advocates that the association between size and the mean returns substitute for a more basic association of the economic risk factors and the expected returns. The strongest factor of these people in the explanation of the impact of size is the dissimilarity that exists between the “monthly returns on the low and high- grade corporate bonds” that finds a type of “default risk” in the case of returns that costs.

Similarly, the same investigators support the fact that the association of size with the average return is much of “relative prospects effect.””.In the case of companies that are facing a loss, there is more susceptibility of the prospects of earning towards the factors that decide the economy.

Applications of the Fama-French theory:

The two variables that can easily be assessed are the book to market equity and the size. The model shows that these two variables significantly explain the cross- section of average stock returns. Further validation of this concept greatly depends on whether it is an interpretation of logical or illogical pricing of the assets or its capacity to persist. It is likely that the variables like the book to market equity and the size could explain the cross section of the average return merely by chance In the sample taken by Fama and French, but they are not associated with the expected returns. also there is sufficient proof that the association between the BE and the ME is strong and also same.

The Chen-Zhang Three-factor Model:

This is a recently introduced model that takes into account the factors like “the market factor, a low-minus-high investment factor, and a high-minus-low ROA factor.” The performance of the model regarding the experimental results is excellent. Though the model incorporates only three factors as its major constituents, it is different from the Fama-French model in the sense that it tends to note many aspects that the Fama-French model fails to answer and equally performs like the Fama-french model. Chen and Zhang take the rational approach could be used in the situations like assessing the performance of the mutual funds, evaluating expected returns for the allotment of the assets, assessing the abnormal returns, scheming the costs of equity for stock assessment and budgeting the capital. The applications mentioned above are greatly dependent on the accuracy of the model used. Moreover, the intuition provided by the q- theory shows that the predictability of the model can be used in the future as well. More importantly, this model also explains the thrifty explanation of the “cross-section of expected stock returns.”

Merits

The major difference between the Fama-French model and the three- factor model is that the Fama- French model considers the SMB and HML as the causative factors especially in the light of ICAPM or APT, whereas in contrast, the SMB and HML are not considered as risk factors in the three- factor model. Also, the q-theory gives room to connect the expected returns and the characteristic features of the firm sensibly economically without presuming to misprice. Some investigators make use of mispricing as a substitute for market equity. However, the factors devised in the three- factor model are conceived on economic bases which are not influenced by mispricing.

De-merits:

The major shortcomings of the model are that the tests are only instinctively inspired from the q-theory and are not a definite structural assessment of the theory. Also, the q-theory does not suggest anything about the behavior of the investors which can turn out to be either coherent or in-coherent. The tests conducted would not be able to differentiate whether the incongruity is because of logical reasons or just due to behavioral aspects.

Also, this model has just compared the covariance and characteristic features and concluded that on the adjustment of the investment-to-assets, there is no association between the investment factor loadings and the average returns. However, on adjusting for investment factor loadings, the explaining capacity of the investment to assets is not changed. Likewise, on adjusting for ROA, there is no association between the average returns and the ROA factor loadings, but it is to be noted that the explaining capacity of the ROA. This proof shows that the declined investment stocks and the elevated ROA stocks yield greater average returns. This happens irrespective of the situation- if they possess same patterns of return or more ROA stocks and less investment. Moreover the factor loadings the greater returns related to the less investment and more ROA stocks more than the magnitude of the loadings performing as substitutes for the features.

Conclusions:

Thus, the models are consistent with the Daniel and Titman model but inconsistent with the Fama-French model. As mentioned earlier, the ROA factor loadings are interpreted as non-risk factors, and the model also provides a thrifty explanation of the cross-sectional returns. The authors are of the opinion that if there is significance for a factor in the method of cross-sectional regressions, then it is possible that it could yield the same significance by the time series regressions also. Factor loadings and characteristics are supposed to be equally primitive. The hypothesis of Daniel and Titman is supposed to be little too strong by this model. Hypothetically the q-theory gives an estimate of the collection of associations among the expected returns and the characteristics. The simplistic acquisition of the equation is not derived from the concept of mispricing and is significantly in agreement with the theory of risk. Experimentally, it is possible to imagine that the characteristics provide an accurate assessment of the true beta compared to the estimated betas. Notably, the rolling window regressions are used to calculate the betas and are the mean betas at two years previously to the formation of the portfolios. Subsequent research should be able to identify the different inference and as true betas are almost non-existent in a real life situation, arriving at a judgment is impossible at this stage of the model.

Researchers to mentor-We write your Assignments & Dissertation

With our team of researchers & Statisticians - Tutors India guarantees your grade & acceptance!

About serviceLiu, Zhang and Warner’s view:

The association between the momentum portfolio returns and the changes in the loadings of factors on the rate of growth and the production of the industry are studied by Liu, Zhang, and Warner. From the study, it is evident that the people who are victorious have greater loadings compared to the losers. The spread in the loading is acquired from the greater positive loadings of those who have emerged victorious. Stocks that are small have greater loadings than stocks that are big, and also the value stocks have loadings that are greater than growth stocks. Tests like “standard multifactor tests” are employed in this model and proof that the rate of growth in the sector of industrial production is a causative factor that is priced.

The work done by Liu, Zhang, and Warner shows the link that exists between momentum profits, macroeconomic risk, and factor pricing. They stated that “We focus on the growth rate of industrial production (MP hereafter). This focus is motivated partially by Chen, Roll, and Ross (1986). Their early work argued that MP should be a priced factor. Their tests supported this argument, and have been replicated elsewhere (e.g., Shanken and Weinstein 2006). An additional motivation is that, as documented later, small stocks have higher MP loadings than big stocks, and value stocks have higher MP loadings than growth stocks. This raises the possibility that size and value proxy for common factor risk, and that MP could potentially help explain both the cross section of returns and momentum returns. Our use of a growth-related macroeconomic risk variable to study momentum portfolios is also motivated by the theoretical work of Johnson (2002). He argues that apparent momentum profits can reflect temporary increases in growth related risk for winner-minus-loser portfolios. We present some new results. First, winners have temporarily higher MP loadings than losers. Winner loadings temporarily rise, and loser loadings temporarily fall. For example, in univariate regressions, the loadings for winners and losers in the first month of the holding period following portfolio formation are, 0.63 and −0.17, respectively, but six months later the loadings are similar at about 0.38. Second, most of the high MP loadings occur in high momentum deciles. These loading patterns are predicted by Johnson (2002). Third, MP appears to be a priced risk factor. Depending on model specification, the MP risk premium estimated from Fama-Macbeth (1973) multifactor cross-sectional regressions ranges from 0.11% to 1.29% per month. These various results suggest the potential usefulness of growth related risk variables. While these results could help point the way toward risk-based explanations for the cross section of re-turns, they fall short in one key area, however. In most of our tests, the combined effect of factor pricing and risk shifts does not explain a large fraction of momentum returns. We make no claim that our results have solved the momentum puzzle (e.g., Jegadeesh and Titman 1993). The role of MP remains an open question because the risk premium estimates are sensitive to test procedure”.

Findings:

The results of the work done by Liu, Zhang, and warner show that the risk factors that are associated to the growth are much more useful though these results may not be useful in the assessment of the nature of the “risk-based explanations for the cross section of re-turns”, there is one particular aspect that is not assessed by them.

In much of the evaluations done, the total effect of the factor pricing and the shifts in the risk is not explained by a great fraction of the momentum. Liu, Zhang and Warner futher state that “We make no claim that our results have solved the momentum puzzle. However, the inability of our tests to explain momentum is due, in part, to a low estimated MP risk premium. The magnitude of the estimated premium is sensitive to test procedure. Higher estimates reported in Shanken and Weinstein (2006) appear sufficient to explain winner-minus-loser returns. Thus, the role of MP-related risk is still an open question”.

The recent problems existing in the financial sectors predict a much better power of explanation. It is assumed that with proper hindsight changes in stock prices can be explained by general methodic influences and also influences from the industry and also the events that are specific to the company. The work done by Roll provided an experimental probe into the issue.

Regressions found in the case of individual returns in the monthly stock on one index in the market or many factors also gave power of explanation as assessed by the mean controlled value of R2 in the proximity of 0.30. On addition of a factor of industry, the average was increased to above 0.35.

As stated by Roll, “For the decile of the largest AMEX and NYSE firms, the portfolios of smaller firms were constructed to match each large firm in aggregate size. These portfolios of smaller firms were constructed to match each large firm in aggregate size. These portfolios had much bigger R2s Than their corresponding size-matched large individual firms; thereby indicating that diversification by the large firm is not much of an explanation for the slightly larger explanatory power. There was no perceptible cross-sectional relation between the R2 of the large firm and the R2 of its aggregate size matched portfolio”.

As well the portfolios were made to make a match betweem a sample of big firms in the sense of both volume and industry. More over, only less association exists between the variables like size and the power of explanation. What is more surprising is the fact that there was literally no association in cross sectional terms between the value of R2 of an company that is greatly matched to its size and that which is matched to its industry portfolio.This goes on to show that the power of the industry by methodic factors of the economy is very much likely to be similar across a range of industries.

Data that was collected daily was used to assess the incidence and the influence of the specific information on a company. With the availability of daily data, the mean value of R2 of the similar set of big companies came down by a factor of around 0.20. Every time the company is cited in the wall street journal or the “Dow jones Broad Tape” was taken as an event that gives information. Regression analyses on the methodic factors were being done solely using the “non-information dates”. Even, using this data that has been sensored on information, the mean power of explanation could be made only little better, For instance, by the use of multiple factor APT pervasive factors as those that regress the mean R2 was elevated from 0.205 to 0.225 by using each and every day in the years betweem 1982 till 1986. This was done after the exclusion of the event of information before two days and after two days.

However, there was a great decrease in the kurtosis of the sample from the exclusion of the news events that are public. A simplistic combination of models of distribution gave rise to two results.

- The mean minium ratio of “news variance to background noise variance” was over a factor of 20 for all dates of sample but it averages to only over a factor of 7 for dates without any news

- The calculated probability of the information was mediocre, but the available material for recognizable dates of public news and for other dates as well. This greatly seems to imply that there exists either private news or “occasional frenzy unrelated to concrete information”

Full Fledged Academic Writing & Editing services

Original and high-standard Content

Plagiarism free document

Fully referenced with high quality peer reviewed journals & textbooks

On-time delivery

Unlimited Revisions

On call /in-person brainstorming session

More From TutorsIndia

Coursework Index Dissertation Index Dissertation Proposal Research Methodologies Literature Review Manuscript DevelopmentREQUEST REMOVAL