The US and the UK Master’s Part / Chapter-wise Dissertation Writing Service

Then You’ve Certainly Reached the Right place

Indian banking industry

Chapter 1 - Introduction

KYC - “KNOW YOUR CUSTOMERS”

“CUSTOMER” - WHO IS HE

“A customer is the most important person in any business

A customer is not dependent upon us. We are dependent upon him.

A customer is not an interruption of our work. He is the sole purpose of it.

A customer does us a favor when he comes in. We aren't doing him a favor by waiting on him.

A customer is an essential part of our business--not an outsider.

A customer is not just money in the cash register. He is a human being with feelings and deserves to be treated with respect.

A customer is a person who comes to us with his needs and his wants. It is our job to fill them.

A customer deserves the most courteous attention we can give him. He is the lifeblood of this and every business. He pays your salary. Without him we would have to close our doors. Don't ever forget it” (Porter, )

1.1 INDUSTRY PROFILE

GENERAL BANKING

Iin the banking companies act,1949 a banking company in India has been defined.as one “which transacts the business of banking which means the accepting, for the purpose of lending or investment of deposits of money from the public, repayable on demand or otherwise and withdraw able by cheque, draft, order or otherwise.” The above definition derives most of the activities a Bank performs. Certain other ancillary activities which are ancillary to this business of accepting deposits and lending are allowed to the banks to perform. Therefore, with the public the bank ‘s relationship revolves around accepting deposits and lending money. Transfer of money - both domestic and foreign - from one place to another is another activity which is is assuming increasing importance. In banking parlance this activity is generally known as "remittance business". The involvement of buying and selling foreign currencies generally called forex (foreign exchange) business is largely a part of remittance albeit.

FUNCTIONING OF A BANK

The most complicated of corporate operations is the functioning of a Bank . Governments in most countries regulate this sector severely as banking involves dealing directly with money. Of corporate operations the most complicated is the functioning of a bank . The present condition of banks in India is due to the traditionally and very strict regulations in the opinion of certain quarters, where NPAs are of a very high order. Financial reforms, which started in 1991 has a lot to be done although cleared all the cobwebs.The operations are made even more complicated, sometimes bordering on illogical due to the multiplicity of policy and regulations that a Bank has to work with. An overview of the functions in as simple manner as possible is dealt with in this section, which is intended for banking professional.The banking Regulation Act of India, 1949 defines Banking as "accepting, for the purpose of lending or investment of deposits of money from the public, repayable on demand or otherwise and withdraw able by cheques, draft, and order or otherwise."

Overview of the Banking Industry

In the last decades of the 18th century banking in India originated . the largest and oldest commercial bank of existence in the country is the State Bank of India a government-owned bank that traces its origins back to June 1806 .

The oldest bank in existence in India is the State Bank of India, a government-owned bank that traces its origins back to June 1806 and that is the largest commercial bank in the country.

Central banking is the responsibility of the Reserve Bank of India, which in 1935 formally took over these responsibilities from the then Imperial Bank of India, relegating it to commercial banking functions.

After India's independence in 1947, the Reserve Bank was nationalized and given broader powers. In 1969 the government nationalized the 14 largest commercial banks; the government nationalized the six next largest in 1980.

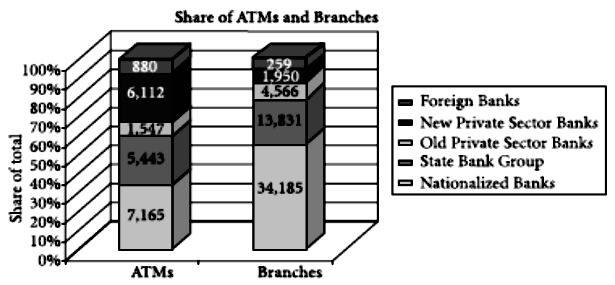

Currently, India has 88 scheduled commercial banks (SCBs) - 27 public sector banks (that is with the Government of India holding a stake), 29 private banks (these do not have government stake; they may be publicly listed and traded on stock exchanges) and 31 foreign banks. They have a combined network of over 53,000 branches and 17,000 ATMs. According to a report by ICRA Limited, a rating agency, the public sector banks hold over 75% of total assets of the banking industry, with the private and foreign banks holding 18.2% and 6.5% respectively.

EARLY HISTORY

Banking in India originated in the last decades of the 18th century. The first banks were The General Bank of India, which started in 1786, and the Bank of Hindustan, both of which are now defunct. The oldest bank in existence in India is the State Bank of India, which originated in the Bank of Calcutta in June 1806, which almost immediately became the Bank of Bengal. This was one of the three presidency banks, the other two being the Bank of Bombay and the Bank of Madras, all three of which were established under charters from the British East India Company. For many years the Presidency banks acted as quasi-central banks, as did their successors. The three banks merged in 1925 to form the Imperial Bank of India, which, upon India's independence, became the State Bank of India. Indian merchants in Calcutta established the Union Bank in 1839, but it failed in 1848 as a consequence of the economic crisis of 1848-49. The Allahabad Bank, established in 1865 and still functioning today, is the oldest Joint Stock bank in India.. The depositors lost money and lost interest in keeping deposits with banks. Subsequently, banking in India remained the exclusive domain of Europeans for next several decades until the beginning of the 20th century. Foreign banks too started to arrive, particularly in Calcutta, in the 1860s. The presidency banks dominated banking in India but there were also some exchange banks and a number of Indian joint stock banks. All these banks operated in different segments of the economy. By the 1900s, the market expanded with the establishment of banks such as Punjab National Bank, in 1895 in Lahore and Bank of India, in 1906, in Mumbai - both of which were founded under private ownership. Punjab National Bank is the first Swadeshi Bank founded by the leaders like Lala Lajpat Rai, Sardar Dyal Singh Majithia. The Swadeshi movement in particular inspired local businessmen and political figures to found banks of and for the Indian community.

A number of banks established then have survived to the present such as Bank of India, Corporation Bank, Indian Bank, Bank of Baroda, Canara Bank and Central Bank of India.

The first bank in India, though conservative, was established in 1786. From 1786 till today, the journey of Indian Banking System can be segregated into three distinct phases.

They are as mentioned below:

- Early phase from 1786 to 1969 of Indian Banks

- Nationalization of Indian Banks and up to 1991 prior to Indian banking sector Reforms.

- New phase of Indian Banking System with the advent of Indian Financial & Banking Sector Reforms after 1991.

Phase I

The General Bank of India was set up in the year 1786. Next came Bank of Hindustan and Bengal Bank. The East India Company established Bank of Bengal (1809), Bank of Bombay (1840) and Bank of Madras (1843) as independent units and called it Presidency Banks. These three banks were amalgamated in 1920 and Imperial Bank of India was established which started as private shareholders banks, mostly Europeans shareholders. In 1865 Allahabad Bank was established and first time exclusively by Indians, Punjab National Bank Ltd. was set up in 1894 with headquarters at Lahore. Between 1906 and 1913, Bank of India, Central Bank of India, Bank of Baroda, Canara Bank, Indian Bank, and Bank of Mysore were set up. Reserve Bank of India came in 1935. During the first phase the growth was very slow and banks also experienced periodic failures between 1913 and 1948. There were approximately 1100 banks, mostly small. To streamline the functioning and activities of commercial banks, the Government of India came up with The Banking Companies Act, 1949 which was later changed to Banking Regulation Act 1949 as per amending Act of 1965.

Phase II

Government took major steps in this Indian Banking Sector Reform after independence.

In 1955, it nationalized Imperial Bank of India with extensive banking facilities on a large scale especially in rural and semi-urban areas.

It formed State Bank of India to act as the principal agent of RBI and to handle banking transactions of the Union and State Governments all over the country. Seven banks forming subsidiary of State Bank of India was nationalized in 1960 on 19th July, 1969, major process of nationalization was carried out.

- First phase of nationalization 14 major commercial banks in the country were nationalized.

- Second phase of nationalization Indian Banking Sector Reform was carried out in 1980 with seven more banks.

This step brought 80% of the banking segment in India under Government ownership. The following are the steps taken by the Government of India to Regulate Banking Institutions in the Country:

- 1949 : Enactment of Banking Regulation Act.

- 1955 : Nationalization of State Bank of India.

- 1959 : Nationalization of SBI subsidiaries.

- 1961 : Insurance cover extended to deposits.

- 1969 : Nationalization of 14 major banks.

- 1971 : Creation of credit guarantee corporation.

- 1975 : Creation of regional rural banks.

- 1980 : Nationalization of seven banks with deposits over 200 crore.

After the nationalization of banks, the branches of the public sector bank India rose to approximately 800% in deposits and advances took a huge jump by 11,000%. Banking in the sunshine of Government ownership gave the public implicit faith and immense confidence about the sustainability of these institutions.

Phase III

This phase has introduced many more products and facilities in the banking sector in its reforms measure. In 1991, under the chairmanship of M Narasimham, a committee was set up by his name which worked for the liberalization of banking practices. The country is flooded with foreign banks and their ATM stations. Efforts are being put to give a satisfactory service to customers. Phone banking and net banking is introduced. The entire system became more convenient and swift. Time is given more importance than money. The financial system of India has shown a great deal of resilience. The customers have more choices in choosing their banks. A competition has been established within the banks operating in India. With stiff competition and advancement of technology, the service provided by banks has become more easy and convenient. The past days are witness to an hour wait before withdrawing cash from accounts or a cheque from north of the country being cleared in one month in the south.

FROM WORLD WAR I TO INDEPENDENCE

Until the independence of India were challenging for Indian banking, the period during the First World War (1914-1918) through the end of the Second World War (1939-1945), and two years thereafter. Despite the Indian economy gaining indirect boost due to war-related economic activities the years of the First World War were turbulent, and it took its toll with banks simply collapsing . Between 1913 and 1918 as indicated in the following table At least 94 banks in India failed :

| Years | Number of banks that failed | Authorized capital(Rs. Lakhs) | Paid-up Capital (Rs. Lakhs) |

|---|---|---|---|

| 1913 | 12 | 274 | 35 |

| 1914 | 42 | 710 | 109 |

| 1915 | 11 | 56 | 5 |

| 1916 | 13 | 231 | 4 |

| 1917 | 9 | 76 | 25 |

| 1918 | 7 | 209 | 1 |

POST-INDEPENDENCE

Paralyzing banking activities for months The partition of India in 1947 adversely impacted the economies of Punjab and West Bengal, . The end of a regime of the Laissez-faire for the Indian banking is marked by India’s independence. The Industrial Policy Resolution adopted by the government in 1948 envisaged a mixed economy and the Government of India initiated measures to play an active role in the economic life of the nation, Including banking and finance this resulted into greater involvement of the state in different segments of the economy

In order to regulate banking major steps included:

- The Reserve bank of India became an institution owned by the Government of India as in 1948, the Reserve Bank of India, India's central banking authority, was nationalized.

- In 1949, the Banking Regulation Act was enacted which empowered the Reserve Bank of India (RBI) "to regulate, control, and inspect the banks in India was empowered by the Banking Regulation Act was enacted in 1948.

- No two banks could have common directors and no new bank or branch of an existing bank could be opened without a license from the RBI is provided by the Banking Regulation Act.

Banks in India except the State Bank of India, continued to be operated and owned by private persons despite these provisions, control and regulations. With the nationalization of major banks in India on 19 July, 1969 this has got changed .

NATIONALIZATION

The Indian banking industry has become an significant tool to facilitate the progress of the Indian economy by the 1960s. Indian banking industry has emerged as a large employer, and a debate has ensued about the possibility to nationalize the banking industry simultaneously.

In the annual conference of the All India Congress Meeting in a paper entitled "Stray thoughts on Bank Nationalization" was expressed by Indira Gandhi,, the-then Prime Minister of India expressed the intention of GOI. With positive enthusiasm the paper was received. GOI issued an ordinance and nationalized the 14 largest commercial banks with effect from the midnight of July 19, 1969 and thereafter, her move was sudden and swift . Description of the step as a "masterstroke of political sagacity" was made by Jayaprakash Narayan, a national leader of India. The Parliament passed the Banking Companies (Acquisition and Transfer of Undertaking) Bill, and it received the presidential approval on 9 August, 1969 within two weeks of the issue of the ordinance,.

In 1980, a second dose of nationalization of 6 more commercial banks followed. To provide the government more control of credit delivery is the stated reason for the nationalization . The GOI controlled around 91% of the banking business of India with the second dose of nationalization.. The government merged New Bank of India with Punjab National Bank later on, in the year 1993,. There was a drastic decrease in the number of nationalized banks from 20 to 19 due to the fact that it was the only merger between nationalized banks. Closer to the average growth rate of the Indian economy the nationalized banks grew at a pace of around 4%, after this, until the 1990s.

To have assisted the Indian economy withstand the global financial crisis of 2007-2009 the nationalized banks were credited by some including Home minister P. Chidambaram,.

LIBERALIZATION

A policy of liberalization, licensing a small number of private banks was adopted by the Narasimha Rao Government in the early 1990s . Global Trust Bank was included and these came to be known as New Generation tech-savvy banks (the first of such new generation banks to be set up), which later merged with Oriental Bank of Commerce, UTI Bank(now re-named as Axis Bank), HDFC Bank and ICICI Bank. Revitalization of the banking sector in India, which has observed rapid growth with strong contribution from all the three sectors of banks, namely, foreign banks, private banks and government banks took place because of this move, along with the rapid growth in the economy of India,

Where all Foreign Investors in banks may be given voting rights which could exceed the present cap of 10%,at present it has gone up to 49% with some limitations, the next stage for the Indian banking has been setup with the proposed relaxation in the norms for Foreign Direct Investment,.

Banking sector in India was fully shaken by this new policy. 4-6-4 method (Borrow at 4%; Lend at 6%; Go home at 4) of functioning was the method accustomed by bankers until this time.

Tech-savvy methods of working for traditional banks were introduced along with a modern look by the fresh wave. . Apart from receiving more, people also demanded more from their banks and all of this led to the retail boom in India.

Even though reach in rural India still remains a challenge for the foreign banks and private sector and presently (2007), banking in India is generally fairly mature In terms of reach-oven, product range supply, product range and reach. Indian banks are considered to have clean, strong and transparent balance sheets in comparison to other banks in comparable economies in its region in terms of quality of assets and capital adequacy, With minimal pressure from the government, the Reserve Bank of India is an autonomous body,. Nevertheless, without any fixed exchange rate-and this has mostly been true, the stated policy of the Bank on the Indian Rupee is to manage volatility.

With the growth in the Indian economy expected to be strong for quite some time-especially in its services sector, the demand for banking services, especially, mortgages, investment services and retail banking are expected to be strong. Asset sales. M&As, takeovers may also be expected by one.

To increase its stake in Kotak Mahindra Bank (a private sector bank) to 10%. In March 2006, the Reserve Bank of India allowed Warburg Pincus. Since the RBI announced norms in 2005 that any stake exceeding 5% in the private sector banks would need to be vetted by them, this is the first time an investor has been allowed to hold more than 5% in a private sector bank.

With regard to loan recovery efforts in connection with personal loans ,vehicles loans and house advances, in recent years critics have charged that the non-government owned banks are too aggresive. Driving defaulting borrowers to suicide are the press reports that the banks' loan recovery efforts have made.

INDIAN BANKING INDUSTRY

From the survey by GOVT in nationalized banks in 2007

- Describing the performance of the banking Industry as “Very Good” by 84 percent of the survey respondents

- Making the PSBs more profitable and competitive by the newly granted autonomy

- Technological upgradation was considered followed by Consolidation in the banking industry

- Increasing the international competitiveness of the Indian banks as key factors currently required.

- Consideration of the HRD related issues as one of the biggest challenge in the process of consolidation by private and public sector banks.

- For the profitability of the banks, customer retention is significantly important.

- Ensuring the security of customer information and stricter security policies to safeguard and feelings of the need of advanced security software’s.

- The biggest challenges that could affect the future growth of Retail banking is the identification of Rising Indebtedness followed by lack of Technological advancements.

- Further in the area of Micro Credit financing, banks intend to increase their exposure further.

Company Profile of SBI

India's largest commercial bank is STATE BANK OF INDIA (SBI). One-fifth of deposits and loans of all scheduled commercial banks in India is commanded by SBI and it has a vast domestic network of over 9000 branches (approximately 14% of all bank branches.

.Numerous non-banking subsidiaries providing insurance, primary dealership in government securities, factoring services, fund management and merchant banking services along with a network of eight banking subsidiaries are included in the State bank Group.

VISION

“MY SBI FIRST IN CUSTOMER SATISFACTION

MY CUSTOMER FIRST

MY SBI”

MISSION

- “We will be prompt, polite and proactive with customers.

- We will be speak the language of young India. We will create products and services that help our customers achieve their goals.

- We will go beyond the call of duty to make our customer feel valued.

- We will be of service even in the remotest part of our country.

- We will offer excellence in service to those abroad as much as we do to those in India.

- We will imbibe state of art technology to drive excellence”.

VALUES

- “We will always be honest, transparent and ethical.

- We will respect our customers and fellow associates.

- We will be knowledge driven.

- We will learn and we will share our learning.

- We will never take the easy way out. We will do everything we can to contribute to the community we work in.

- We will nurture pride in India.”

The eight banking subsidiaries are:

- “State Bank of Bikaner and Jaipur (SBBJ)

- State Bank of Hyderabad (SBH)

- State Bank of India (SBI)

- State Bank of Indore (SBIR)

- State Bank of Mysore (SBM)

- State Bank of Patiala (SBP)

- State Bank of Saurashtra (SBS)

- State Bank of Travancore (SBT)”

When the Bank of Calcutta (later called the Bank of Bengal) was established, the origins of State Bank of India date back to 1806. To form the Imperial Bank of India, the Bank of Bengal and two other Presidency banks (Bank of Madras and Bank of Bombay) were amalgamated in 1921 . State Bank of India (SBI) came into existence by an act of Parliament as successor to the Imperial Bank of India and the controlling interest in the Imperial Bank of India was acquired by the Reserve Bank of India in 1955.. Network of branches spanning all time zones is consisted by the SBI and currently State Bank of India (SBI) has spread its arms around the world . Through its four wings - International Services division, the Foreign Department, , the Foreign Offices division, the Domestic division , SBI's International Banking Group delivers the full range of cross-border finance solutions

Largest bank in India is the State Bank of India (SBI) (LSE: SBID). SBI is the largest bank in the world if one measures by the number of branch offices and employees. In the Indian subcontinent ,Bank of Calcutta, is the oldest commercial bank established in 1806 . Through its vast network in India and overseas SBI provides various domestic, international and NRI products and services,. It is a regional banking sector with an asset base of $126 billion and its reach. With the Reserve Bank of India taking a 60% ownership stake, the government nationalized the bank in 1955. The bank has focused on three priorities in recent years, 1), changing the attitude of its employees (through an ambitious programme aptly named 'Parivartan' which means change) as a large number of employees are very rude to customers. 2) reducing its huge staff through Golden handshake schemes known as the Voluntary Retirement Scheme, which saw many of its best and brightest defect to the private sector, 3. computerizing its operations

HIGHLIGHTS OF ATM PROJECT: as on MARCH 07

- SBI group (No of ATM) : 8460

- Avg daily hits : 30400

- Avg cash availability : 95%

- Customer loyalty score awarded to SBI ATMs better than ICICI & HDFC.

Roots

The State Bank of India traces its roots to the first decade of 19th century, when the Bank of Calcutta, later renamed the Bank of Bengal, was established on 2 June 1806. The government amalgamated Bank of Bengal and two other Presidency banks, namely, the Bank of Bombay (incorporated on 15 April 1840) and the Bank of Madras on 27 January 1921, and named the reorganized banking entity the Imperial Bank of India. All these Presidency banks had been incorporated as joint stock companies, and were the result of the royal charters. The Imperial Bank of India continued as a joint stock company. Until the establishment of a central bank in India the Imperial Bank and its early predecessors served as India's central bank, at least in terms of issuing the currency. The State Bank of India Act 1955, enacted by the Parliament of India, authorized the Reserve Bank of India, which is the central banking organization of India, to acquire a controlling interest in the Imperial Bank of India, which was renamed the State Bank of India on 30 April 1955.

Timeline

- June 2, 1806: The Bank of Calcutta established.

- January 2, 1809: This became the Bank of Bengal.

- April 15, 1840: Bank of Bombay established.

- July 1, 1843: Bank of Madras established.

- 1861: Paper Currency Act passed.

- January 27, 1921: all three banks amalgamated to form Imperial Bank of India.

- July 1, 1955: State Bank of India formed; becomes the first Indian bank to be nationalized.

- 1959: State Bank of India (Subsidiary Banks) Act passed, enabling the State Bank of India to take over eight former State-associated banks as its subsidiaries.

- 1980s When Bank of Cochin in Kerala faced a financial crisis, the government merged it with State Bank of India.

- June 29, 2007: The Government of India today acquired the entire Reserve Bank of India (RBI) shareholding in State Bank of India (SBI), consisting of over 314 million equity shares at a total amount of over 355 billion rupees.

ASSOCIATE BANKS

There are seven other associate banks that fall under SBI. They all use the "State Bank of" name followed by the regional headquarters' name. These were originally banks belonging to princely states before the government nationalized them in 1959. In tune with the first Five Year Plan, emphasizing the development of rural India, the government integrated these banks with the State Bank of India to expand its rural outreach. The State Bank group refers to the seven associates and the parent bank. The group is merging all the associate banks into SBI, which will create a "mega bank", and one hopes, streamline operations and unlock value.

- State Bank of Bikaner & Jaipur

- State Bank of Hyderabad

- State Bank of Indore

- State Bank of Mysore

- State Bank of Patiala

- State Bank of Saurashtra

- State Bank of Travancore

Foreign Offices

State Bank of India is present in 32 countries, where it has 84 offices serving the international needs of the bank's foreign customers, and in some cases conducts retail operations. The focus of these offices is India-related business.

Foreign Branches

SBI has branches in these countries

| Australia | Republic of Maldives |

| Bahrain | Singapore |

| Bangladesh | South Africa |

| Belgium | Sri Lanka |

| Canada | Sultanate of Oman |

| Dubai | The Bahamas |

| France | U.K. |

| Germany | U.S.A |

| Hong Kong | Japan |

| Israel | People's Republic of China |

GROWTH

Mumbai, India location.

State Bank of India has often acted as guarantor to the Indian Government, most notably during Chandra Shekhar's tenure as Prime Minister of India. With more than 9400 branches and a further 4000+ associate bank branches, the SBI has extensive coverage. Following its arch-rival ICICI Bank, State Bank of India has electronically networked most of its metropolitan, urban and semi-urban branches under its Core Banking System (CBS), with over 4500 branches being incorporated so far. The bank has the largest ATM network in the country having more than 5600 ATMs [1]. The State Bank of India has had steady growth over its history, though the Harshad Mehta scam in 1992 marred its image. In recent years, the bank has sought to expand its overseas operations by buying foreign banks. It is the only Indian bank to feature in the top 100 world banks in the Fortune Global 500 rating and various other rankings. According to the Forbes 2000 listing it tops all Indian companies.

IT INITIATIVES

State Bank of India launched a project in 2002 to network more than 14,000 domestic and 70 foreign offices and branches. The first and the second phases of the project have already been completed and the third phase is still in progress. As of December 2006, over 10,000 branches have been covered. The new infrastructure serves as the bank's backbone, carrying all applications, such as the IP telephone network, ATM network, Internet banking and internal e-mail. The new infrastructure has enabled the bank to further grow its ATM network with plans to add another 3,000 by the end of 2007 raising the total number to 8,600. As of September 20, 2007 SBI has 7236 ATMs.

CORPORATE DETAILS

This site provides comprehensive information on State Bank of India or SBI Bank, the premier Nationalized Indian Bank. State Bank of India is actively involved since 1973 in non-profit activity called Community Services Banking. State Bank of India is India's largest bank amongst all public and private sector banks operating in India.

Joint ventures

- SBI Life Insurance Company Ltd (SBI LIFE).

ACTIVITIES

State Bank of India administrative structure is well equipped to oversee the large network of branches in India and abroad. The State Bank of India 14 Local Head Offices and 57 Zonal Offices are located at important cities spread throughout the country. State Bank of India has 52 foreign offices in 34 countries across the globe. The Corporate Accounts Group is a Strategic Business Unit of the Bank set up exclusively to fulfill the specialized banking needs of top corporate in the country.

The main activities of are into –

| Personal Banking. | Corporate |

| NRI Services. | SME |

| Agriculture | Domestic Treasury. |

| International |

State Bank of India offers the following services to its customers –

| Broking Services | Safe Deposit Lockers. |

| Revised Service Charge. | Foreign Inward Remittances. |

| ATM Services. | E-Pay |

| Internet Banking. | E-Rail |

Moreover, State Bank of India has Colleges/Institutes/Training Centers that are the seats of learning and research and development. It caters not only to the employees of State Bank of India but also other banks/establishments in India and abroad.

Performance

SBI Bank India had Total Income of Rs 68376.83 crore for the financial year 2006 -07. State Bank of India has posted Net Income to the tune of Rs 6364.38 crore or the financial year 2006 -07.

Organization

State Bank of India is headed by Mr. Shri O. P. Bhatt, Chairman.

Researchers to mentor-We write your Assignments & Dissertation

With our team of researchers & Statisticians - Tutors India guarantees your grade & acceptance!

Our servicesObjective for the Study

PRIMARY OBJECTIVE

- A study on impact of implementation of 12 hours banking in SBI, Mahindra city branch.

SECONDARY OBJECTIVE

- To study the satisfaction level of customers in the SBI bank.

- To ascertain the perceptions of customers regarding the service quality in SBI Bank.

- To understand services provided to customers by SBI Bank.

- To identify the areas which need improvement in quality of service.

- To create awareness of different banking services offered among the customers of SBI.

- To give Suggestions to improve the services.

1.4 NEED FOR STUDY

Because of the following reasons, I prefer this project work to get the knowledge of the banking system.

- Banking is an essential industry.

- It is where we often wind up when we are seeking a problem in financial crisis and money related query.

- Banking is one of the most regulated businesses in the world.

- Banks remain important source for career opportunities for people.

- It is vital system for developing economy for the nation.

- Banks can play a dynamic role in delivery and purchase of consumer durables.

SCOPE OF STUDY

In an environment where the customer has come to the central stage, regular and comprehensive appraisal of Bank services in relation to the perceptions of customers are of much importance. Because of the information explosion today’s customer is more knowledgeable and the expectations are very high. In order to satisfy them better service is needed. The first step to marketing is to identifying the needs of the customers and the level of satisfaction towards the existing services. The study of customer satisfaction will provide the insight in to the weak areas of customer service and make corrective steps. Client loyalty not only improves efficiency, but it also enhances business. A customer loyalty strategy that involves tailoring services to individual client’s need has the additional benefit of not causing damage. For this 12 hrs banking will help this branch to improve better service and yield customer loyalty. Moreover the study will be of much use to Bankers in framing their future marketing strategies.

LIMITATIONS OF THE STUDY

- Since the time is less the researcher has taken a sample of 120 people and it will not reveal the whole population of a country.

- The study is limited to a particular branch of SBI bank.

- It is possible that some of the respondents may have perceived the study as being backed by the management and thus the reliability of their response is questionable.

- Due to lack of time, respondents would have carelessly marked the questionnaire resulting in inaccuracy of data

CHAPTER 2 - REVIEW OF LITERATURE

The banking sector in India has made remarkable progress since the economic reforms in 1991. New private sector banks have brought the necessary competition into the industry and spearheaded the changes towards higher utilization of technology, improved customer service and innovative products. Customers are now becoming increasingly conscious of their rights and are demanding more than ever before. The recent trends show that most banks are shifting from a “product-centric model” to a “customer-centric model” as customer satisfaction has become one of the major determinants of business growth. In this context, prioritization of preferences and close monitoring of customer satisfaction have become essential for banks. Keeping these in mind, an attempt has been made in this study to analyze the factors that are essential in influencing the investment decision of the customers of the public sector banks. For this purpose, Factor Analysis, which is the most appropriate multivariate technique, has been used to identify the groups of determinants. Factor analysis identifies common dimensions of factors from the observed variables that link together the seemingly unrelated variables and provides insight into the underlying structure of the data. Secondly, this study also suggests some measures to formulate marketing strategies to lure customers towards banks.

Key Words

Bank: A bank is a financial institution whose primary activity is to act as a payment agent for customers and to borrow and lend money. It is an institution for receiving, keeping, and lending money.

Mobile Banking: Mobile banking (also known as M-Banking, mbanking, SMS Banking etc.) is a term used for performing balance checks, account transactions, payments etc. via a mobile device such as a mobile phone. Mobile banking today (2007) is most often performed via SMS or the Mobile Internet but can also use special programs called clients downloaded to the mobile device.

Core Banking System: Core Banking is a general term used to describe the services provided by a group of networked bank branches. Bank Customers may access their funds and other simple transactions from any of the member branch offices.

ATM: An automated teller machine (ATM) is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller. On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smartcard with a chip, that contains a unique card number and some security information, such as an expiration date or CVC (CVV). Security is provided by the customer entering a personal identification number (PIN).

Using an ATM, customers can access their bank accounts in order to make cash withdrawals (or credit card cash advances) and check their account balances as well as purchasing mobile cell phone prepaid credit. ATMs are known by various other names including automated banking machine, money machine, bank machine, cash machine$,

RTGS: (Real Time Gross Settlement)

- Transferring fund from one bank to another.

- Launched in 26th March 2004

- In Indian currencies only.

- Privacy & security is guaranteed.

- Minimum amount Rs10, 00,000

- Quick transfer - Maximum 2 hours.

- Not for intra bank transactions

NEFT – (National Exchange fund transfer)

- Fund transfer - Less than 10,00,000Rs.

- Quick transfer

INTERNET BANKING

Online banking (or Internet banking) allows customers to conduct financial transactions on a secure website operated by their retail or virtual bank, credit union or building society.

A channel for receiving information and delivering their products / services to customers through internet.

1. Disseminate information

- Different products and services

- Placing queries

2. Fund based transactions

- Fund transfer

- Bills payment

- Transact purchase

- Scale of securities

- Requisition of cheque book

- Stop payment of cheque

NORMAL BANKING TRANSACTIONS

- Funds transfer self accounts

- Third party transfer

- New account opening

- D D request

- Standing instructions

- New cheque book request etc.

VALUE ADDED SERVICES

- Railway ticket booking

- Bill payments

- Insurance premium payments

- Mutual funds investments

- Credit card payments

- Tax payments

- Use your 3 in 1 account to trade online

- RTGS & NEFT payments

Key facts

- Internet banking facility available to both retail & corporate customers.

- Customers can operate their accounts all across India.

- It removes restrictions imposed by geography & time.

- It enables the customers to carry out their banking activities from their desktop.

- Both normal banking transactions & value added services on online.

Highlights

- Implemented in 9112 domestic branches.

- No of corporate INB customers crossed 1000.

- Campaign / events to familiarize customers with security features.

TARGET: growth of 40 to 50 % in branches under INB & 60 % growth in customer registration.

Risk associated with Internet banking:

- Operational risk

- Security risk

- Cross border risk

- Legal risk

- Traditional risk

- Cyber crime

Operational risk

- Inaccurate processing of transaction.

- Non-enforceability of contract.

- Data integrity, privacy, confidentiability.

- Weakness of design, implemented & monitoring information system.

Security risk

- Unauthorized access, risk management system, portfolio management system.

- Loss of reputation

- Infringing customer privacy

Cross border risk

- Beyond national border

- Different rules & regulations

Legal risk

- Violation of (or) non-conformance with law, rules & regulation.

Traditional risk

- Credit, liquidity, risk

- Interest rate, market risk

Cyber crime

- Hacking of customer user account

Deregulations, innovations in mobile and wireless technologies and media convergence, together with the rapid diffusion of the Internet, have opened up strategic business opportunities in the financial sector. With deregulation removing entry barriers, an increasing number of online banks are threatening the market share of ‘bricks and mortar’ banks. To survive this competition, and to leverage the new opportunities of online and mobile banking facilitated by the Internet, many banks have adapted a hybrid, ‘clicks and mortar’ model, to increase their profitability while reducing transaction costs. Banking and investment have been revolutionaries by the rapid diffusion of the Internet. As a response to globalization and deregulation of financial markets and increased competition from non-bank financial institutions and online banks.

This model is becoming increasingly popular because of its perceived ability to lower costs, create new revenue streams and augment existing distribution channels. Internet banking gains momentums, decreasing switching costs make consumer loyalties harder to retain banking demonstrates the attributes of an oligopoly, making use of use risk avoidance and relatively undifferentiated customer service approaches. One of the major factors affecting the banks is the changing need and perceptions of the consumer. Increasingly, consumers expect online services from their financial institutions and electronic delivery of services is becoming a necessity. Banks are using the Internet as a strategic weapon, leveraging it as a distribution channel to offer complex products at the same quality they can provide from their physical branches, at a lower cost, to more potential customers, without boundaries. The online channel enables banks to offer low-cost, high value-added financial services and also benefit from the promotional opportunity to cross-sell products such as credit cards and loans. Online transaction costs can be as low as 1 % of an equivalent off-line transaction, rapidly increasing the popularity of the online option with consumers, as well as banks. In saving time and money for users, banks offer online banking as a less expensive alternative to branch banking. In addition, online banking enables banks to acquire information on consumer habits and preferences, for later marketing purposes. An expanding customer base and transaction cost savings are major benefits for banks.

The lack of brand awareness and recognition is still an issue with Internet-only banks, which carry liquidity risks and may be subject to panic withdrawals. Pricing for individual services such as fee-per-chequeing transaction or per-transfer may also still be an issue.

Although physical banks are increasingly charging such fees – removing the distinction between the offerings of the two types. Another innovation which has had an impact on banks is the rapidly evolving concept of mobile banking. The simple concept of banking on handheld devices such as mobile phones is becoming more popular, as it leverages Internet connectivity to bring convenience to consumer’s finger tips.

Customer confidence and comfort levels seem to increase when banking online with a known ‘bricks and mortar’ brand name. Banks appear to have a distinct advantage where they offer a range of integrated services – leveraging the Internet and mobile networks.

Economy-specific issues and consumer attitudes do have an impact on banking models. In this section we broadly review the banking sector movements towards the ‘clicks and mortar’ model of banking, through technological innovations and shifting consumer attitudes in India.

The convenience these systems provide has resulted in more than 50% of banking transactions (such as withdrawals, account management, deposits) being conducted outside bank branches with consequent financial benefits to the banks themselves.

Problems with this technology

- Islands of applications in the branches of a bank, with dissimilar computers, operating systems and application packages. There’s no integration of such application and hence forcing the manual intervention.

- Due to various flavors of hardware and software, no data integrity could be maintained even though the application was for the same business purpose. Ex: No one could see a unified picture of overall deposits, loans customer information etc of the whole Bank.

- Due to dissimilar application packages, Inter branch reconciliation and communication was not possible. Even if it was made possible, it was not straight through.

- Still some banks are continuing with this technology which is very out dated

- Not able to trust vendors, banks relied on half vendor based software and half in-house software. They couldn’t integrate the two, without some manual intervention.

Due to the above problems, banks are still dependent on manual procedures only. More than 50% of the process of generating MIS from the branches and send to their Central Office required manual intervention.

This technology helped banks, only to lessen some burden on back office. It couldn’t achieve

- Better monitoring control

- Better decision making

- Faster service delivery

- Better performance

- New products or services etc

Instead of alleviating the threats posed by manual banking, it actually increased them further, leaving lot of confusion on whom to make accountable, the computer or the computer operator.

Some of the new fraud techniques that surfaced due to computerization

- Intentionally writing programs to siphon off the funds

- Illegal transactions between accounts

- Wrong interest calculations

WORK HOUR PROGRAM related to 12 hours banking

CRM provides:

A distinctive & consistent customer experience, clear identification of the organization, technology & process related capability prioritization of these capabilities.

Benefits of variable work hour

Companies are recognizing that employees have lives outside the company (workspace) and by providing the flexibility to accommodate family needs, leisure activities, and other obligation.

Benefits for company

- Increased employee productivity

- Increased employee morale

- Reduced parking demand and congestion around worksite

- Reduced employee turnover, absenteeism and tardiness

- Extended work hrs allow you to serve customers @ different time zones

- Greater ability to recruit and retain working parents.

Benefits for employee

- Improved job satisfaction

- Reduced commuting time and stress

- More flexibility for leisure activities

- Opportunities to work during peak productivity hours

- Better able to manage personnel and professional responsibilities

Types of variable work hour

- Flex - time includes maxi – flex

- Compressed work hour

- Staggered work hour

Companies have to take care of

- Core timing

- Monitoring timing

How can a company choose their variable work timing?

For that they have to depend upon

- What type of work employees do?

- How does employee interact with customers?

- How much internal coordination is required?

- Management style?

- Back up support available?

12-hour banking becomes more common now

Banking is getting more convenient. You don't always have to jostle with the crowds at the counter during the peak hour. Now you can walk into some bank branches at a late evening hour or even on a Sundays. A number of banks have extended their working hours in select branches. A decade ago, banks were open for public transactions for any four hours between 8.30 a.m and 2.30 p.m, depending on local convenience. This was extended by about two hours a few years ago. Now, bank branches being open for 12 hours and more are getting common.

A couple of branches of IndusInd Bank have started banking on Sundays. ICICI, Bank of Boroda offers 8 a.m to 8 p.m banking at many of its branches. Not always have these extended hours been introduced by banks to cater to increased traffic. Sometimes the bank is trying to convey a subtle message with the symbolism of extended hours - that it cares for its customers. Most of our customers prefer coming to the branch but cannot make it during normal business hours. The traffic of the customers is very high during the evening hours.

However, extended banking hours does not work at every place. With advanced technology, banking transactions can take place very easily and hardly adds up to the cost. Therefore, on Sunday, our branch will have only few staff members and 8-8 banking will have staff members on a rotational basis. Some public sector banks too had started 8-8 banking a few years ago. The largest bank, State Bank of India, started extended banking hours at some metro branches seven years ago. However, with the increasing number of ATMs, a customer's dependence on a bank's branch has reduced considerably. There are only a few customers who visit the branch for enquiries and cheque collections during the extended hours in certain branches. some branch managers have said that there are fewer footfalls at bank's branches during the extended hours.

CUSTOMER SERVICE

When we talk about services @ banking, we must also look for

1. Tangibility

- Modernized facilities @ bank

- Professional appearance of staffs

- Materials availability

2. Reliability

- Promise to do something in certain time

- Bank show sincere interest in solving customer problem

- Performing right service from first time

- Error free records

3. Responsiveness

- Intimation about transaction performed

- Prompt service to customers @ any time

- Respond to customer request

4. Assurance

- Knowledge & courtesy of employee

- Ability of staff to convey

5. Empathy

- Individual attention

- Operating hour convenience

- Understand specific needs

CHAPTER 3 - RESEARCH METHODOLOGY

SAMPLING DESIGN

Target population

- The target population in this research refers to the bank customers

- The respondents are mixed (gender/ income level/occupation/education level).

Sampling unit

- Customers of SBI bank

Sampling method

- Non-probability sampling.

Sample size

- Ghauri (2002) stated that: sample size depend on the desired precision from the estimate. Precision is the size of the estimating interval when the problem is one of estimating a population parameter”.

- 120 respondents as the sample size due to limited of time

Sampling plan

- The research is going to collect the data from the ATMS and also by visiting the bank.

SOURCES OF DATA

PRIMARY DATA

The data is basically primary in nature; it was obtained from the customers

SECONDARY DATA

Secondary data are those, which are collected from the already existing information through reference. The secondary data are collected by analyzing various materials like Com¬pany profiles, Magazines, Journals, Past records and reports and websites.

Data Collection Method

- Our communication approach was basically structured questioning, that is personal interview with the aid of printed questionnaires.

DATA ANALYSIS – STATISTICAL TOOL USED

Appropriate statistical analysis will be adopted.

- PERCENTAGE ANALYSIS

- CORRELATION

- CHI-SQUARE

- ANOVA

- RANKING

The data will be tabulated and analyzed.

CHAPTER 4 – DATA ANALYSIS & INTERPRETATION

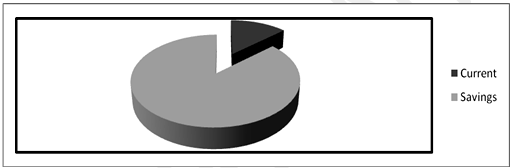

A/C TYPE

| Account type | No of respondent | % |

|---|---|---|

| Current | 16 | 13.3 |

| Savings | 104 | 86.7 |

| Total | 120 | 100 |

Chart 1

INFERENCE

From the table we understood that out of 120 customers, 86.7% are handling saving account with this branch and 13.3 % are handling current account.

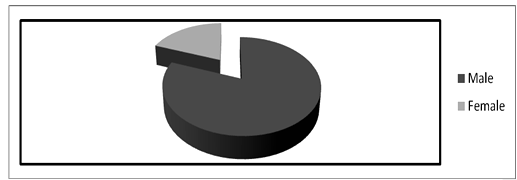

GENDER

| Gender | No of respondent | % |

|---|---|---|

| Male | 97 | 80.8 |

| Female | 23 | 19.2 |

| Total | 120 | 100 |

Chart 2

INFERENCE

Out of 120 customers, 80.8% are male and 19.2% are female who handle accounts in this branch.

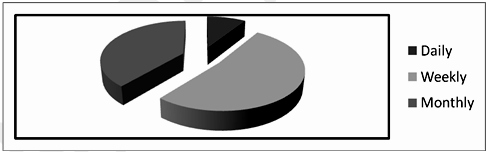

VISIT TO BANK

| Visit to bank | No of respondent | % |

|---|---|---|

| Daily | 11 | 9.17 |

| Weekly | 63 | 52.5 |

| Monthly | 46 | 39.33 |

| Total | 120 | 100 |

Chart 3

INFERENCE

From this we come to know that out of 120 customers, 52.5% customers visit the bank weekly for their work to be done, 39% visit the bank once in a month and remaining come daily.

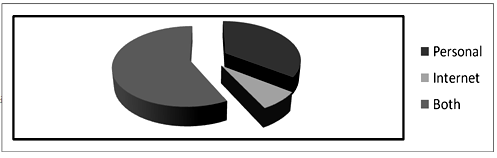

BANKING PREFERENCE

| Bank preference | No of respondent | % |

|---|---|---|

| Personal | 42 | 35 |

| Internet | 9 | 7.5 |

| Both | 69 | 57.5 |

| Total | 120 | 100 |

Chart 4

INFERENCE: From this we come to know that 57.5% of customers use both internet banking and personnel banking for their transaction to be done. 35% of customers use only use Personnel banking. 7.5% of customers use only internet banking.

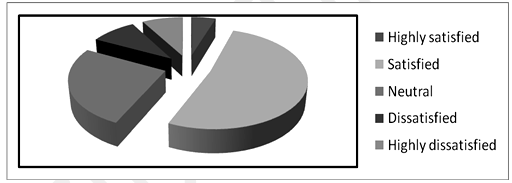

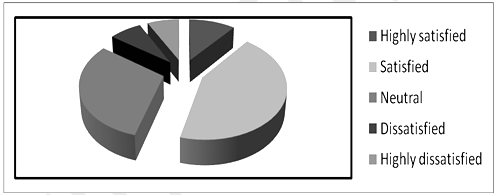

1. CURRENT BRANCH FUNCTION:

| Branch function | No of respondent | % |

|---|---|---|

| Highly satisfied | 6 | 5 |

| Satisfied | 62 | 51.7 |

| Neutral | 31 | 25.8 |

| Dissatisfied | 11 | 9.17 |

| Highly dissatisfied | 10 | 8.3 |

| Total | 120 | 100 |

Chart 5

INFERENCE

From this we come to know that about 5% customers are highly satisfied, 51.7% of them were satisfied, 25 % have neutral opinion about the branch functioning and 17.4 % were not satisfied.

RANKING

2. PREFERENCE IN CHOOSING THIS BANK

Table 1

CRM = (9*4) + (27*3) + (39*2) + (45*1) = 240--------------------------------------------VII

Loyalty = (66*7) + (27*6) + (21*5) + (4*4) = 745-----------------------------------------I

Trust = (27*7) + (24*6) + (30*5) + (33*4) + (6*1) = 621---------------------------------IV

Technology = (9*5) + (24*4) + (57*3) + (9*2) + (21*1) = 378--------------------------VI

Integrity = (39*7) + (54*6) + (15*5) + (12*4) = 720--------------------------------------II

| Preference in choosing this bank | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| CRM | - | - | - | 9 | 27 | 39 | 45 |

| LOYALTY | 66 | 27 | 21 | 4 | - | - | - |

| TRUST | 27 | 24 | 30 | 33 | - | - | 6 |

| TECHNOLOGY | - | - | 9 | 24 | 57 | 9 | 21 |

| INTEGRITY | 39 | 54 | 15 | 12 | - | - | - |

| LONG EXISTANCE | 24 | 33 | 51 | 6 | 6 | - | - |

| MORE NO OF BRANCHES | 15 | 18 | 24 | 48 | 6 | 9 | - |

Long existence = (24*7) + (33*6) + (51*5) + (6*4) + (6*3) = 663----------------------III

More no of branches = (15*7) + (18*6) + (24*5) + (48*4) + (6*3) + (9*2) = 561----V

INFERENCE

Loyalty, integrity & long existence were top 3 preferences in choosing this bank from the opinion of 120 customers

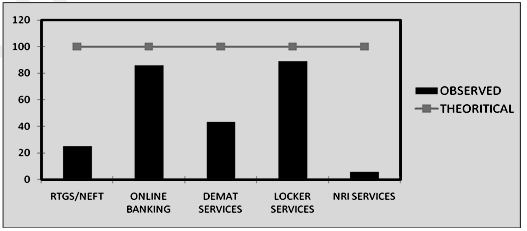

3. AWARENESS ABOUT DIFFERENT SERVICE

| Services offered | Observed | Theoretical |

|---|---|---|

| RTGS/NEFT | 30/120=25 | 100 |

| ONLINE BANKING | 103/120=85.83 | 100 |

| DEMAT SERVICES | 52/120=43.33 | 100 |

| LOCKER SERVICES | 107/120=89.17 | 100 |

| NRI SERVICES | 7/120=5.83 | 100 |

Chart 6

INFERENCE

From the above data we come to know that, 89.17% of customers were aware of Locker service, 85.83 % of customers were of aware of Internet banking, 43.33% of customers were of aware of DEMAT services, 25% of customers were of RTGS/NEFT and 5.83% of customers were aware of NRI services.

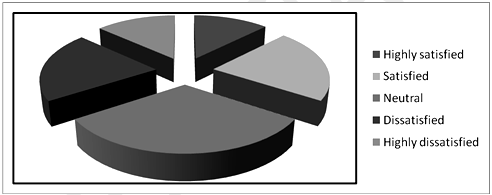

4. QUALITY OF SERVICE

| Quality of service | No of respondent | % |

|---|---|---|

| Highly satisfied | 22 | 18.33 |

| Satisfied | 61 | 50.83 |

| Neutral | 26 | 21.67 |

| Dissatisfied | 8 | 6.67 |

| Highly dissatisfied | 3 | 2.5 |

| Total | 120 | 100 |

Chart 7

INFERENCE

From this we come to know that about 18.33% of customers are highly satisfied, 50.83% were satisfied, 21.67 % have neutral opinion about the quality of service offered and 9.1 % were not satisfied.

5. STAFF HANDING

| Staff handling | No of respondent | % |

|---|---|---|

| Highly satisfied | 24 | 20 |

| Satisfied | 39 | 32.5 |

| Neutral | 41 | 34.17 |

| Dissatisfied | 8 | 6.67 |

| Highly dissatisfied | 8 | 6.67 |

| Total | 120 | 100 |

Chart 8

INFERENCE

From this we come to know that about 20% of customers are highly satisfied, 32.5% were satisfied, 34.17 % have neutral opinion about the staff handling offered and 13.33 % were not satisfied.

6. BRANCH SPACIOUS

| No of respondent | % | |

|---|---|---|

| Highly satisfied | 45 | 37.5 |

| Satisfied | 48 | 40 |

| Neutral | 12 | 10 |

| Dissatisfied | 8 | 6.67 |

| Highly dissatisfied | 7 | 5.83 |

| Total | 120 | 100 |

Chart 9

INFERENCE

From this we come to know that about 37.50% of customers are highly satisfied, 40% were satisfied, 10 % have neutral opinion about the branch spacious offered and 12.5 % were not satisfied.

7. PROFESSIONAL APPEARANCE

| No of respondent | % | |

|---|---|---|

| Highly satisfied | 26 | 21.67 |

| Satisfied | 27 | 22.5 |

| Neutral | 41 | 34.17 |

| Dissatisfied | 12 | 10 |

| Highly dissatisfied | 14 | 11.67 |

| Total | 120 | 100 |

Chart 10

INFERENCE

From this we come to know that about 21.67% of customers are highly satisfied, 22.5% were satisfied, 34.17 % have neutral opinion about the professional appearance offered and 21.67 % were not satisfied.

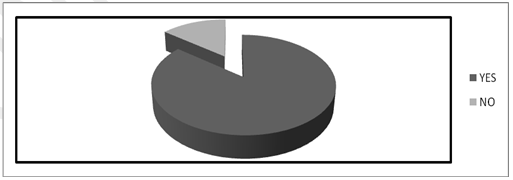

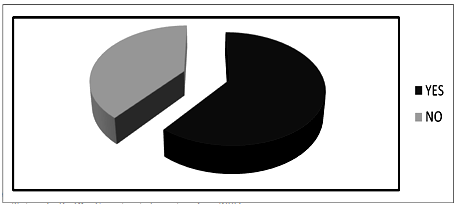

8. AWARENESS OF INTERNET BANKING

| Awareness | No of respondent | % |

|---|---|---|

| YES | 103 | 85.83 |

| NO | 17 | 14.17 |

| Total | 120 | 100 |

Chart 11

INFERENCE

From this we come to know that only 85.83% of customers were aware of internet banking offered by bank.

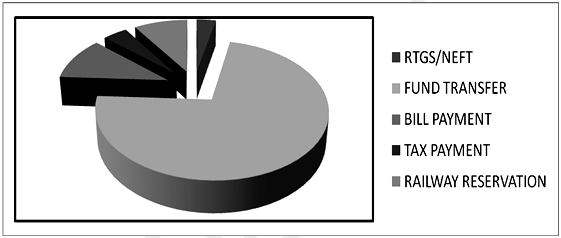

9. SERVICES IN INTERNET BANKING

| Services | No of respondent | % |

|---|---|---|

| RTGS/NEFT | 4 | 3.33 |

| FUND TRANSFER | 87 | 72.5 |

| BILL PAYMENT | 13 | 10.8 |

| TAX PAYMENT | 5 | 4.17 |

| RAILWAY RESERVATION | 11 | 9.17 |

| Total | 120 | 100 |

Chart 12

Inference

From this we come to know that 72.5% of customers were aware of fund transfer, 10.8% were aware of bill payment, 9.17% were aware of Railway reservation, 5% were aware of tax payment and 3.33% were aware of RTGS/NEFT.

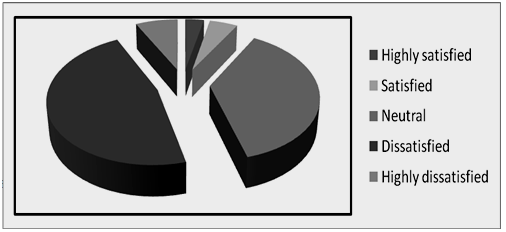

10. SATISFACTION OF INTERNET BANKING

| Internet banking | No of respondent | % |

|---|---|---|

| Highly satisfied | 4 | 3.33 |

| Satisfied | 6 | 5 |

| Neutral | 45 | 37.5 |

| Dissatisfied | 56 | 46.67 |

| Highly dissatisfied | 9 | 7.5 |

| Total | 120 | 100 |

Chart 13

INFERENCE

Only 8.3% of customers were satisfied with internet banking, about 37.5 % have neutral opinion and 54.3% were dissatisfied.

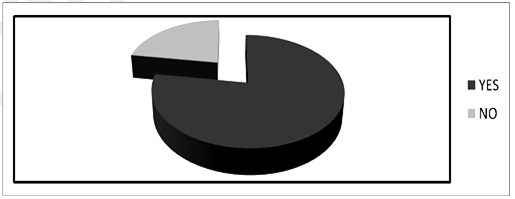

11. ATM AVIALABILITY NEAR YOUR LOCALITY

| ATM availability | No of respondent | % |

|---|---|---|

| YES | 111 | 92.5 |

| NO | 9 | 7.5 |

| Total | 120 | 100 |

Chart 14

INFERENCE

From this we come to know that 92.5% of customers were satisfied with ATM availability.

12. EASE OF USE OF ATM

| No of respondent | % | |

|---|---|---|

| YES | 93 | 77.5 |

| NO | 27 | 22.5 |

| Total | 120 | 100 |

Chart 15

INFERENCE

From this we come to know that 77.5 % of customers were satisfied with ease of use.

13. ATM FUNCTIONING

| ATM functioning | No of respondent | % |

|---|---|---|

| Highly satisfied | 27 | 22.5 |

| Satisfied | 43 | 35.83 |

| Neutral | 18 | 15 |

| Dissatisfied | 15 | 12.5 |

| Highly dissatisfied | 17 | 14.17 |

| Total | 120 | 100 |

Chart 16

INFERENCE

From the data we come to know that 22.5% of customers were highly satisfied, 35.83% were satisfied, 15% have neutral opinion and 26.67% were dissatisfied.

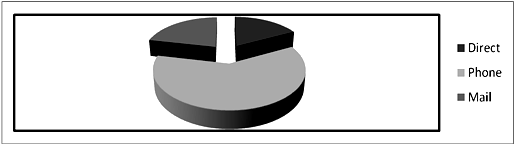

14. PLACING YOUR ORDER

| Placing your order | No of respondent | % |

|---|---|---|

| Direct | 21 | 17.5 |

| Phone | 73 | 60.83 |

| 26 | 21.67 | |

| Total | 120 | 100 |

Chart 17

INFERENCE

From the data we come to know about 60.83% of customer place the queries through Phone, 17.5% of them through mail and remaining personally.

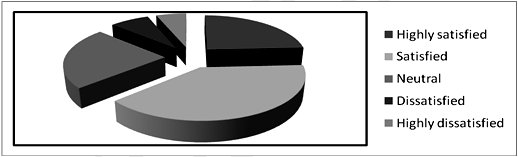

15. OVERALL QUERIES HANDLING

| No | % | |

|---|---|---|

| Highly satisfied | 29 | 24.17 |

| Satisfied | 47 | 39.17 |

| Neutral | 28 | 23.33 |

| Dissatisfied | 9 | 7.5 |

| Highly dissatisfied | 7 | 5.8 |

| Total | 120 | 100 |

Chart 18

INFERENCE

From the data we come to know that 24.17% of customers were highly satisfied, 39.17% were satisfied, 23.33% have neutral opinion and 13.2% were dissatisfied.

RANKING

16. PREFERENCE IN THIS BRANCH

Table 2

| Preference in this branch | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Speed of transaction | 32 | 11 | 52 | 17 | 8 |

| Bahavioural aspect | 11 | 39 | 26 | 32 | 12 |

| Low service charge | 26 | 28 | 37 | 17 | 12 |

| Low pricing | 42 | 31 | 19 | 16 | 12 |

| Branch ambience | 21 | 63 | 17 | 17 | 2 |

SPEED OF TRANSACTION = (32*5) + (11*4) + (52*3) + (17*2) + (8*1) = 402------- III

BAHAVIOURAL ASPECT = (11*5) + (39*4) + (26*3) + (32*2) + (12*1) = 365------- V

LOW SERVICE CHARGE = (26*5) + (28*4) + (37*3) + (17*2) + (12*1) = 399-------- IV

LOW PRICING = (42*5) + (31*4) + (19*3) + (16*2) + (12*1) = 435--------------------- II

BRANCH AMBIENCE = (21*5) + (63*4) + (17*3) + (17*2) + (2*1) = 444------------- I

INFERENCE

Branch ambience, low pricing and speed of transaction were top 3 preferences in choosing this branch from the opinion of 120 customers.

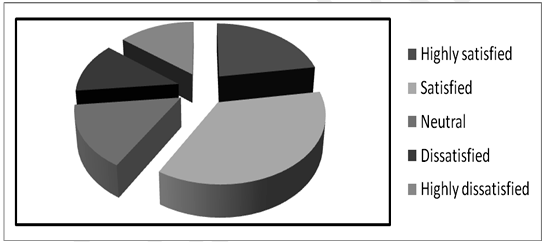

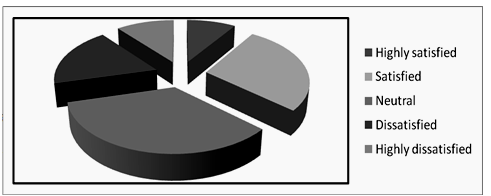

18. OVERALL SATISFACTION

| Overall satisfaction | No | % |

|---|---|---|

| Highly satisfied | 13 | 10.83 |

| Satisfied | 52 | 43.33 |

| Neutral | 37 | 30.83 |

| Dissatisfied | 9 | 7.5 |

| Highly dissatisfied | 9 | 7.5 |

| Total | 120 | 100 |

Chart 19

INFERENCE

From the data we come to know that 10.83% of customers were highly satisfied, 43.33% were satisfied, 30.83% have neutral opinion and 15% were dissatisfied.

12 HOURS BANKING

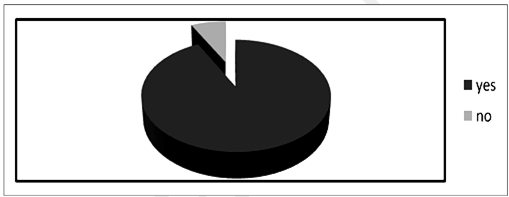

19. IMPLEMENTATION OF 12 HOURS BANKING - IMPROVE BUSINESS

| IMPROVE BUSINESS | No | % |

|---|---|---|

| YES | 73 | 60.83 |

| NO | 47 | 39.17 |

| Total | 120 | 100 |

Chart 20

INFERENCE

From the data we come to know that about 60.83% of customers have positive opinion that implementation 12 hrs banking will improve business.

20. IMPLEMENTATION OF 12 HOURS BANKING - EXPLOIT RESOURCE

| EXPLOIT RESOURCE | No | % |

|---|---|---|

| Highly agree | 15 | 12.5 |

| Agree | 26 | 21.67 |

| Neutral | 38 | 31.67 |

| Disagree | 25 | 20.83 |

| Highly disagree | 16 | 13.33 |

| Total | 120 | 100 |

Chart 21

INFERENCE

From the data we come to know that 12.5% of customers were highly agree, 21.67% were agree, 31.67% have neutral opinion and 34.16% were disagree with implementation of 12hrs banking exploit resource.

21. IMPLEMENTATION OF 12 HOURS BANKING - BURDEN TO STAFF

| BURDEN TO STAFF | No | % |

|---|---|---|

| Highly agree | 11 | 9.17 |

| Agree | 33 | 27.5 |

| Neutral | 41 | 34.17 |

| Disagree | 22 | 18.33 |

| Highly disagree | 13 | 10.83 |

| Total | 120 | 100 |

Chart 22

INFERENCE

From the data we come to know that 9.17% of customers were highly agree, 27.5% were agree, 34.17% have neutral opinion and 19.16% were disagree with implementation of 12 hrs banking will be burden to staff.

22. IMPLEMENTATION OF 12 HOURS BANKING - AVOID TRANSACTION

| AVOID TRANSACTION | No | % |

|---|---|---|

| Highly agree | 11 | 9.17 |

| Agree | 22 | 18.33 |

| Neutral | 39 | 32.5 |

| Disagree | 29 | 24.17 |

| Highly disagree | 19 | 15.83 |

| Total | 120 | 100 |

Chart 23

INFERENCE

From the data we come to know that 9.17% of customers were highly agree, 18.33% were agree, 32.5% have neutral opinion and 40% were disagree with implementation of 12 hrs banking avoid transaction.

23. IMPLEMENTATION OF 12 HOURS BANKING - IMPROVE SERVICE QUALITY

| IMPROVE SERVICE QUALITY | No | % |

|---|---|---|

| Highly agree | 43 | 35.83 |

| Agree | 47 | 39.7 |

| Neutral | 12 | 10 |

| Disagree | 10 | 8.33 |

| Highly disagree | 8 | 6.67 |

| Total | 120 | 100 |

Chart 24

INFERENCE

From the data we come to know that 37.5% of customers were highly agree, 40% were agree, 10% have neutral opinion and 12.5% were disagree with implementation of 12 hrs banking improve service quality.

24. IMPLEMENTATION OF 12 HOURS BANKING - IMPROVE CUSTOMER LOYALTY

| IMPROVE CUSTOMER LOYALTY | No | % |

|---|---|---|

| Highly agree | 41 | 34.17 |

| Agree | 33 | 27.5 |

| Neutral | 19 | 15.83 |

| Disagree | 17 | 14.17 |

| Highly disagree | 10 | 8.33 |

| Total | 120 | 100 |

Chart 25

INFERENCE

From the data we come to know that 25.83% of customers highly agree, 40.83% of them agree 19.17 were neutral in their opinion and 14% of them disagree with implementation of 12 hours banking improvement in customer loyalty.

25. IMPLEMENTATION OF 12 HOURS BANKING - AFFECT INTERNET BANKING

| AFFECT INTERNET BANKING | No | % |

|---|---|---|

| Highly agree | 15 | 12.5 |

| Agree | 45 | 37.5 |

| Neutral | 36 | 30 |

| Disagree | 10 | 8.33 |

| Highly disagree | 14 | 11.67 |

| Total | 120 | 100 |

Chart 26

INFERENCE

From the data we come to know that 12.5% of customers were highly agree, 37.5 % were agree, 30% have neutral opinion and 20% were disagree with implementation of 12 hours banking affect internet banking.

CHI SQUARE – TYPE 1

26. COMPETE WITH PRIVATE & FOREIGN BANKS VS. IMPLEMENTING 12 HRS BANKING

Ho- there is significant difference between implementation of 12 hrs banking in this branch and other compete ting public, private and foreign banking.

H1- there is significant difference between implementation of 12 hrs banking in this branch and other compete ting public, private and foreign banking.

Table 11

| O | E | (O-E)2 | (O-E)2 / E |

|---|---|---|---|

| 42 | 24 | 324 | 13.5 |

| 37 | 24 | 169 | 7.04 |

| 25 | 24 | 1 | .04 |

| 8 | 24 | 256 | 10.67 |

| 8 | 24 | 256 | 10.67 |

| 41.92 |

CV = 41.92

TV @ df = 5-1 = 4

= 7.78

CV>TV, Accept H1

So, there is significant difference between implementation of 12 hrs banking in this branch and other compete ting public, private and foreign banking.

INFERENCE

This branch will be dependent on other compete ting banks if 12 hrs is implemented.

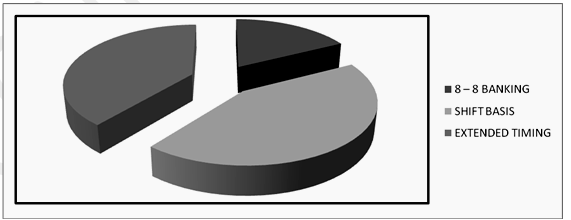

27. IMPLEMENTATION OF 12 HRS BANKING TO IMPROVE BUSINESS

| TIMING | NO OF RESPONDENT | % |

|---|---|---|

| 8 – 8 BANKING | 21 | 17.5 |

| SHIFT BASIS | 52 | 43.33 |

| EXTENDED TIMING | 47 | 39.17 |

| TOTAL | 120 | 100 |

Chart 27

INFERENCE

From the data we come to know 43.33% of customer want shift basis, 39.17% of them wants extended timing and 17.5% want 8-8 banking for their 12 hrs banking to get implemented.

CHI SQUARE: TYPE 1

INTERNET BANKING VS. IMPLEMENTING 12 HRS BANKING

Ho- no significant difference between implementing 12 hrs banking and internet banking

H1- significant difference between implementing 12 hrs banking and internet banking

Table 12

| O | E | (O-E)2 | (O-E)2 / E |

|---|---|---|---|

| 15 | 24 | 81 | 3.37 |

| 45 | 24 | 441 | 18.37 |

| 36 | 24 | 144 | 6 |

| 10 | 24 | 196 | 8.17 |

| 14 | 24 | 100 | 41.17 |

| 77.08 |

CV = 77.08

TV @ df = 5-1 = 4

= 7.78

CV>TV, Accept H1

There is significant difference between implementing 12 hrs banking and internet banking

INFERENCE

Internet banking will get affected if this branch implements 12 hours banking.

CHI SQUARE – TYPE-2

IMPLEMENTING 12 HOURS WILL IMPROVE BUSINESS VS. MAKE ADDITIONAL COST TO BANK

H0- no significant difference between implementing 12 hrs banking to improve business and 12 hrs make additional cost.

H1- significant difference between implementing 12 hrs banking to improve business and 12 hrs make additional cost.

Table 13

Find E,

E (40) = 41.98

E (33) = 31.02

E (29) = 41.98

E (18) = 19.98

| Yes | No | ||

|---|---|---|---|

| Yes | 40 | 33 | 73 |

| No | 29 | 18 | 47 |

| 69 | 51 | 120 |

| O | E | (O-E)2 | (O-E)2 / E |

|---|---|---|---|

| 40 | 41.98 | 39.20 | .093 |

| 33 | 31.02 | 39.20 | .126 |

| 29 | 41.98 | 168.49 | 4.013 |

| 18 | 19.98 | 39.20 | .196 |

| .428 |

Df = (2-1)*(2-1) = 1

TV = 3.841

TV > CV, accept Ho

So, there is no significant difference between implementing 12 hrs banking to improve business and 12 hrs make additional cost.

INFERENCE

Implementation of 12 hrs banking will not incur additional cost to bank.

SUGGESTIONS

- 89.17% of customers were aware of Locker service, 85.83 % of customers were of aware of Internet banking, 43.33% of customers were of aware of DEMAT services, 25% of customers were of RTGS/NEFT and 5.83% of customers were aware of NRI services. This shows that there is communication gap between bank and customers. So marketing strategy should be improved. (Chart 6).

- CRM is not satisfied with customers, so bank has to concentrate on customer relations. (table 1)

- About 47.5 % of customers have neutral and dissatisfaction over staff handling. So proper training should be given to handle customers efficiently, bank also can recruit additional staff to serve better. (chart 8)

- About 90% of customers have neutral and dissatisfied with Internet banking. So bank need to concentrate on ease of usage of internet banking and improvement should be made according to customer expectation. This is the initial stage of usage of internet banking so personnel care should be taken to handle queries regarding usage of internet banking. In future this will increase customer satisfaction regarding usage of internet banking. (chart 13)

- Most of queries were placed through phone were no special staff is there to handle such customer queries. So bank has to take steps to recruit customer care official to handle such queries. (chart 17)

DATA

Several surveys have been done on why customers do not give a business repeat business. Reasons given by customers for not returning for repeat business:

Moved - 4%

Other Friendships - 6%

Competition - 11%

Dissatisfaction - 12%

Employee Attitude - 78% -

Need of CRM in the Banking Industry

A Relationship-based Marketing approach has the following benefits: -

- across the range of financial products / services available, they need to increase thir service.

- Referral sources are the Long-term customers.

- In order to tailor the products, long term relationships are necessary.

How can you differentiate between your satisfied customers and your loyal customers? Here are eight ways. They are equally relevant to your external customers as they are to your internal employee customers.

- Pricing. You negotiate prices with satisfied customers. You negotiate costs with loyal customers.

- Payment. Satisfied customer pay at their discretion. Loyal customers pay on time.

- Referrals. Satisfied customers become referrals of your competitors. Loyal customers willingly provide referrals to you.

- Turnover. Turnover rates of 15% or higher of satisfied customers, less than 5% are out of your control.

- Competitive data.

- Perception. Satisfied customers perceive you as a commodity provide, while loyal customers perceive as a partner.

BENEFITS

- Sustained High growth

- Sustained High Margins

- Loyal and increasing customer base

- Sustained High employee satisfaction

- Scalable, Robust and state-of-art IT infrastructure

- Sustained High Regulatory compliance

- Sustained High investor satisfaction

- Agile business process

CONCLUSION

REASONS TO CHOOSE SBI SERVICE

- Efficient customer service

- Low service charge

- Integrity

- Long existence

- More ATM’s

SERVICES PREFERRED MORE

- ATM SERVICE

- CORE BANKING SYSTEM

These are services which attracted more customers. So this service can be improved by Technological up gradation, Expansion of ATM network, Advertisements, Additional sales force, Market campaign, Door step banking, Additional customer service counters using 12 hours banking, which interns increases customer loyalty.

FUTURE PROJECTS

- To serve U better.

Major focus in future

- Cash / cheque acceptance in ATM

- Fund transfer through ATM

- Request for cheque book through ATM

- RTGS/NEFT trough ATM

- Merge with associated subsidiary baks.

"The success of the economic reforms is therefore all to see and the driving force of these reforms is the Banking sector".

P. CHIDAMBARAM

Former FINANCE MINISTER

QUESTIONNAIRE

Visit to bank: Daily / Weekly / Monthly

A/c type you hold: Current / Savings

How you handle your account? Personal / Internet

GENERAL

1. Are you satisfied with the current branch function & time spent in this branch for your work?

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

2. Please rank your preferences that at what aspect are you linked with this bank?

| Customer relationship management | |

| Loyalty | |

| Trust | |

| Integrity | |

| Technology | |

| Long existence | |

| More no of branches | |

| Brand name |

3.Are you aware of different types of services offered by bank?

- Yes

- No

4. Are you satisfied with the quality of service provided by the bank staff?

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

5. Staffs are in a position to reduce your queuing time in transaction & handle your transaction / problem in time?

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

6. Is the branch spacious

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

7. Professional appearance of staffs

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

8.Are you aware of internet banking service offered by bank?

- Yes

- No

9. Are you satisfied with internet banking in terms of security (transaction & intimation)?

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

10.Is the bank ATM’s available near your locality?

- Yes

- No

11.Is the bank ATM is easy to access?

- Yes

- No

12.Are you satisfied with ATM functioning (in terms of availability of cash, transaction slip)?

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

13. Which among the following is easy in placing your queries to bank?

- Directly

- Phone

14.Your level of satisfaction with the overall queries being handled?

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

15.Which among the following made you choose this branch?

| Speed of transaction | |

| Behavioral aspect | |

| Low Service charges | |

| Low Pricing | |

| Branch ambience | |

| Location |

16.Are there any difficulties you faced while you using internet banking service

18. Overall are you satisfied with the bank?

- Highly Satisfied

- Satisfied

- Neutral

- Dissatisfied

- Highly Dissatisfied

QUESTIONNAIRE

1.Are you aware and whether this branch requires 12 hrs banking?

- Yes

- No

IMPACT AFTER IMPLEMENTATION

2. Will 12 hrs banking exploit resources?

- Highly Agree

- Agree

- Neutral

- Disagree

- Highly Disagree

3.Will 12 hrs banking burden to staff?

- Highly Agree

- Agree

- Neutral

- Disagree

- Highly Disagree

4.Will 12 hrs banking avoid transaction mistakes?

- Highly Agree

- Agree

- Neutral

- Disagree

- Highly Disagree

5. Will 12 hrs banking improve service quality of bank?

- Highly Agree

- Agree

- Neutral

- Disagree

- Highly Disagree

6. Will 12 hrs banking increase customer loyalties?

- Highly Agree

- Agree

- Neutral

- Disagree

- Highly Disagree

7. Will 12 hrs banking affect Internet banking?

- Highly Agree

- Agree

- Neutral

- Disagree

- Highly Disagree

8. Are you aware of 12hrs banking provided by private &foreign banks, can public sector banks compete them in terms of technology?

- Highly Agree

- Agree

- Neutral

- Disagree

- Highly Disagree

9. How it can be implemented?

- 8a.m.-8p.m.

- Shift basis

- Extended timings ‘mention’ ______________

References

www. Statebankofindia.com

Full Fledged Academic Writing & Editing services

Original and high-standard Content

Plagiarism free document

Fully referenced with high quality peer reviewed journals & textbooks

On-time delivery

Unlimited Revisions

On call /in-person brainstorming session

More From TutorsIndia

Coursework Index Dissertation Index Dissertation Proposal Research Methodologies Literature Review Manuscript DevelopmentREQUEST REMOVAL