What Analytical Models Should a master’s Dissertation Apply to Evaluate Lean Management and Cost Efficiency?

What Analytical Models Should a master’s Dissertation Apply to Evaluate Lean Management and Cost Efficiency?

- Home

- How To Article

- What Analytical Models Should a master’s Dissertation Apply to Evaluate Lean Management and Cost Efficiency?

Table of Content

- Importance of Analytical Models in Lean Management Research

- Key Analytical Models for Evaluating Lean Management

- Performance Measurement Models for Cost Efficiency

- Comparative Overview of Analytical Models

- Factors to Consider When Selecting Analytical Models

- Integrating Analytical Models into Dissertation Structure

- Conclusion

What Analytical Models Should a master’s Dissertation Apply to Evaluate Lean Management and Cost Efficiency?

Cost efficiency and lean management are two of the major themes in modern research and operations management and are key considerations for master’s students when selecting analytical models to help evaluate lean practices and cost performance in their dissertations, particularly in Lean Management and Cost Efficiency Analysis in master’s Dissertation topics. Analytical models can turn theoretical concepts into measurements of success by helping master’s students evaluate their organisations’ operational efficiency, waste levels and financial performance.[1]

In this article, we discuss the key analytical models that master’s dissertations can apply to evaluate lean management and cost efficiency and provide practical guidance on how to use them, offering useful insights for MBA dissertation topics and students seeking master’s dissertation help.

1. Importance of Analytical Models in Lean Management Research

Lean strategies and cost reduction options can be evaluated using analytical models. It is helpful for students who are writing master’s level dissertations and wish to use analytical models for the following purposes, including those using a dissertation analysis example for guidance:[2]

- Evaluating the operational performance

- Assessing waste and inefficiencies

- Determining cost savings and productivity

- Assisting in making decisions that are based on evidence

- Providing substantiating credibility to the findings of their dissertation

- Producing a dissertation that is descriptive rather than analytical

If a master ’s-level dissertation does not include appropriate analytical models, it may result in a reduction in legitimate academic impact compared to one that does include such models.

2. Key Analytical Models for Evaluating Lean Management

Lean Management Framework and Value Stream Mapping

![[IG1.1]Lean Management Framework and Value Stream Mapping](https://www.tutorsindia.com/academy/wp-content/uploads/2026/03/Lean-Management-Recreation-Image-1-TI.avif)

Value Stream Mapping (VSM) is a common lean analysis tool that provides a method for researchers to look at their workflow processes and identify waste throughout their operations visually.[3]

The following four areas are used to evaluate value streams:

- Cycle time of the process

- Activities that provide value (add to customer profit) vs. no value (do not add to customer profit)

- Where bottlenecks or delays occur within the process or operation

- Utilisation of resources used within the operation

Using Value Stream Mapping (VSM), students can measure the improvements in process efficiencies and cost reductions by comparing current-state to future-state process maps.

| Six Sigma and DMAIC Model | The DMAIC methodology (Define, Measure, Analyse, Improve, Control) is used to evaluate quality and efficiency in lean processes.

|

| Activity-Based Costing (ABC) Model | Activity-Based Costing (ABC) helps assess the effectiveness of Lean Management by categorising costs by activity rather than department, giving a clearer view of cost drivers.

|

3. Performance Measurement Models for Cost Efficiency

3.1. Balanced Scorecard Approach

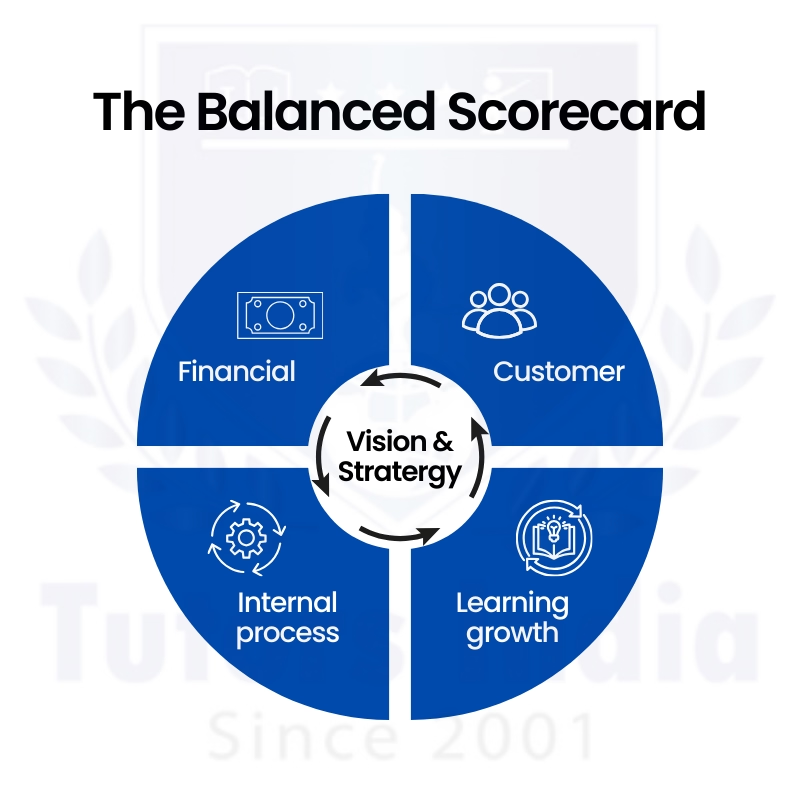

From an organisational perspective, the Balanced Scorecard measures how overall performance is achieved from four different perspectives:

- Financial perspective

- Customer perspective

- Internal Process perspective

- Learning and Growth perspective

It can be used to evaluate how lean initiatives impact financial and operational performance and is often included in dissertation methodology example sections.

3.2. Cost–Benefit Analysis (CBA)

The CBA is a tool to assist with comparing the financial benefit of implementing lean versus the cost of implementing lean. [6]

Examples of information that is used to evaluate ROI, cost savings through waste elimination, productivity gains, and financial impact over the long term.

CBA strengthens financial justification in dissertation research and supports strong analytical justification in MBA dissertation topics focused on operations and finance.

4. Comparative Overview of Analytical Models

Analytical Model | Purpose | Application in Dissertation |

Value Stream Mapping | Process efficiency analysis | Identify waste and delays |

Six Sigma (DMAIC) | Quality and performance improvement | Reduce defects and variation |

Activity-Based Costing | Cost allocation and control | Analyse cost drivers |

Balanced Scorecard | Performance measurement | Evaluate strategic impact |

Cost–Benefit Analysis | Financial evaluation | Measure ROI and savings |

5. Factors to Consider When Selecting Analytical Models

When selecting analytical models for a master’s thesis, students should keep in mind the following things: [7]

- Research objectives and research questions

- Availability and access to data

- The domain or industry being studied

- Quantitative and qualitative methods of analysis

- The demands placed upon them by their supervisor or university

Using multiple complementary models provides a comprehensive understanding of lean management and cost efficiency and helps students overcome dissertation challenges related to analysis.

6. Integrating Models into Dissertation Structure

The methodology and analysis chapters generally include use of analytical models. Students should:

- Validate the selection of models based on available academic literature

- Outline the procedures to collect data

- Implement the model’s systemically

- Evaluate findings of a model critically

- Link the results from the same study with the objectives set out in their research summary.

Clear integration strengthens academic rigor and aligns with expectations for high-quality dissertations and professional dissertation proposal service support.

Conclusion

Analytical models are essential tools for evaluating lean management techniques and cost efficiency in a master’s dissertation. Models such as Value Stream Mapping, Six Sigma, Activity-Based Costing, Balanced Scorecard, and Cost–Benefit Analysis provide a structured framework for evaluating operational and financial performance.

Students can create a strong empirical and methodological foundation using these models. The effective use of analytical frameworks not only strengthens dissertation quality but also supports organisational improvement and practical implementation of lean strategies. With proper guidance and master’s dissertation help, students can successfully apply these models and overcome common research challenges.

What Analytical Models Should a master’s Dissertation Apply to Evaluate Lean Management and Cost Efficiency? [Talk to a Dissertation Expert | Book a Free 15-Minute Consultation]

References

- Tierney, A. A., Shortell, S. M., Rundall, T. G., Blodgett, J. C., & Reponen, E. (2022). Examining the Relationship Between the Lean Management System and Quality Improvement Care Management Processes. Quality management in health care, 31(1), 1–6. https://doi.org/10.1097/QMH.0000000000000318

- Wraae, C. A. D., Opstrup, N., Kyvik, K. O., Brixen, K., & Wien, C. (2024). The use and application of Lean Management methods to research processes-a scoping review protocol. BMJ open, 14(5), e074207. https://doi.org/10.1136/bmjopen-2023-074207

- Morell-Santandreu, O., Santandreu-Mascarell, C., & Garcia-Sabater, J. J. (2021). A Model for the Implementation of Lean Improvements in Healthcare Environments as Applied in a Primary Care Center. International journal of environmental research and public health, 18(6), 2876. https://doi.org/10.3390/ijerph18062876

- de Mast, J., & Lokkerbol, J. (2012). An analysis of the Six Sigma DMAIC method from the perspective of problem solving. International Journal of Production Economics, 139(2), 604–614. https://doi.org/10.1016/j.ijpe.2012.05.035

- Quesado, P., & Silva, R. (2021). Activity-based costing (ABC) and its implication for open innovation. Journal of Open Innovation Technology Market and Complexity, 7(1), 41. https://doi.org/10.3390/joitmc7010041

- Brent R. J. (2023). Cost-Benefit Analysis versus Cost-Effectiveness Analysis from a Societal Perspective in Healthcare. International journal of environmental research and public health, 20(5), 4637. https://doi.org/10.3390/ijerph20054637

- Cárdenas, S., & Valcárcel, M. (2005). Analytical features in qualitative analysis. Trends in Analytical Chemistry: TRAC, 24(6), 477–487. https://doi.org/10.1016/j.trac.2005.03.006